The Tax Hive Free Tax Estimator Calculator is a user-friendly online tool designed to help business owners estimate their tax liabilities. By inputting basic financial information, users can quickly receive an approximation of their business tax obligations. This convenient resource aims to provide clarity and assist in financial planning, making tax time less stressful for entrepreneurs and business owners. This resource is not intended to be a replacement for expert tax advice. To view definitions for the terms used in this calculator, please click here.

Estimated (Quarterly) Tax Payments Calculator

Navigating the world of taxes can be complex, especially when it comes to estimated quarterly tax payments. Whether you’re a freelancer, small business owner, or have multiple sources of income, understanding and managing these payments is crucial.

Use our Estimated Quarterly Tax Payments Calculator to simplify the process and make accurate, timely payments.

What are estimated quarterly tax payments?

Estimated quarterly tax payments are payments made to the Internal Revenue Service (IRS) on income that isn’t subject to withholding taxes. This can include earnings from self-employment, interest, dividends, alimony, rent, gains from the sale of assets, prizes, and awards. Essentially, if you’re earning income that doesn’t have taxes automatically withheld, you’re likely required to pay estimated taxes quarterly to avoid penalties.

How does the estimated quarterly tax payments calculator work?

Our calculator factors your financial situation and IRS rules to calculate an estimate of annual tax payments and balance due. It is based on your entries and could change once other data and documentation are provided.

Who needs to make estimated quarterly tax payments?

Estimated tax payments are typically required for individuals who earn income that is not subject to withholding. This includes earnings from self-employment, interest, dividends, rents, alimony, and other sources. The IRS mandates estimated tax payments for these types of income to ensure that taxpayers are covering their tax liability throughout the year rather than paying everything at once at the end of the year.

The requirement for making estimated tax payments generally applies if you expect to owe at least $1,000 in federal tax after subtracting your withholding and credits, and you expect your withholding and credits to be less than the smaller of 90% of the tax to be shown on your current year’s tax return, or 100% of the tax shown on your previous year’s tax return.

Here are some key points about who needs to make estimated tax payments:

- Self-Employed Individuals: If you are self-employed, you are likely required to make estimated tax payments. This includes freelancers, independent contractors, and small business owners.

- Individuals with Other Sources of Income: If you have income from sources such as interest, dividends, alimony, rent, gains from the sale of assets, prizes, or awards, you may need to make estimated tax payments.

- Taxpayers with Insufficient Withholding: If you are an employee but do not have enough tax withheld from your paycheck or if you have other sources of income on top of your salary, you might need to make estimated tax payments.

- Certain Corporations: Corporations, especially those expecting to owe $500 or more in taxes, typically need to make estimated tax payments.

How to calculate estimated quarterly taxes

Use our calculator

Our Estimated Quarterly Tax Payments Calculator simplifies the estimation process. By inputting your expected annual income, deductions, and credits, the calculator provides an estimated tax payment amount due for the period.

Do it yourself

- Step 1: Estimate taxable income for the year

Start by estimating your total income for the year. This includes all your earnings minus any deductions and exemptions. - Step 2: Calculate income tax

Based on your estimated taxable income, use the current IRS tax brackets to calculate your income tax. You can find your tax bracket using NerdWallet’s 2025-2026 Tax Brackets and Federal Income Tax Rates table. - Step 3: Calculate self-employment tax

If you’re self-employed, calculate your self-employment tax, which covers Social Security and Medicare taxes. The self-employment tax rate is 15.3% of net income. - Step 4: Add it all together, and divide by four

Combine your income tax and self-employment tax, then divide this total by four to get your estimated payment for each quarter.

When are estimated quarterly tax payments due?

Estimated tax payments are due four times a year. The specific due dates typically fall around mid-April, mid-June, mid-September, and mid-January.

- April 15th

- June 17th

- September 16th

- January 15th

How to make estimated quarterly tax payments

Option 1: Get a Tax Hive professional’s help

Tax Hive professionals can help you accurately calculate your estimated quarterly tax payments by considering various factors like your income, deductions, credits, and any recent changes in tax laws to ensure you pay the correct amount. If you have a complex financial situation, such as multiple income streams, investments, or rental properties, or if you’re self-employed, you may want a tax professional to help.

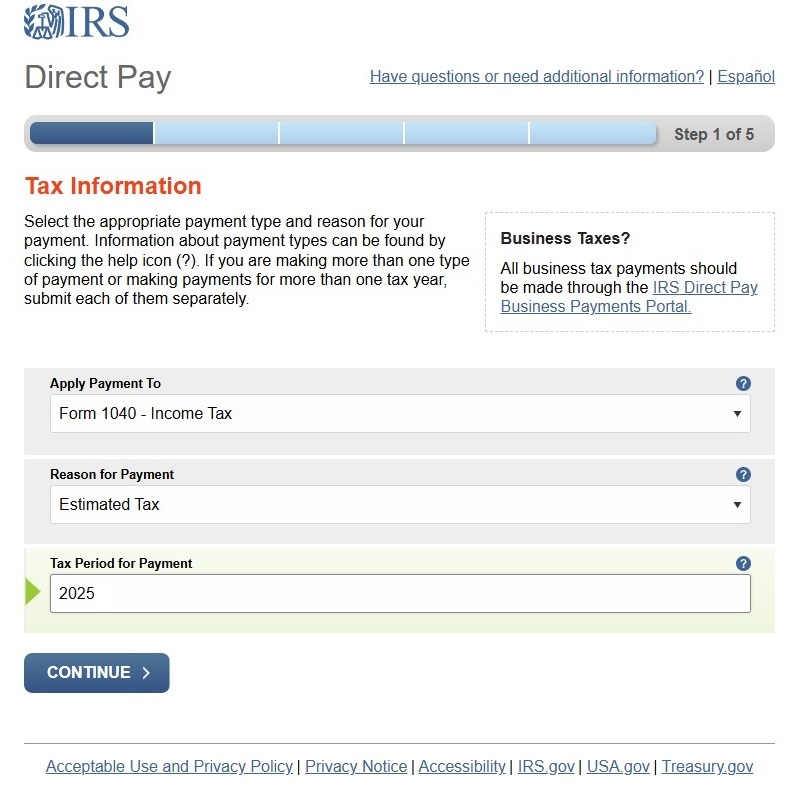

Option 2: Direct Pay

IRS Direct Pay is a convenient, secure, and fee-free method for paying taxes online directly from your bank account. It’s ideal for those seeking a quick and straightforward payment process without the need to create an account or remember additional logins. This service is particularly useful for last-minute payments, offering immediate confirmation and a hassle-free experience while ensuring the safety of your personal information.

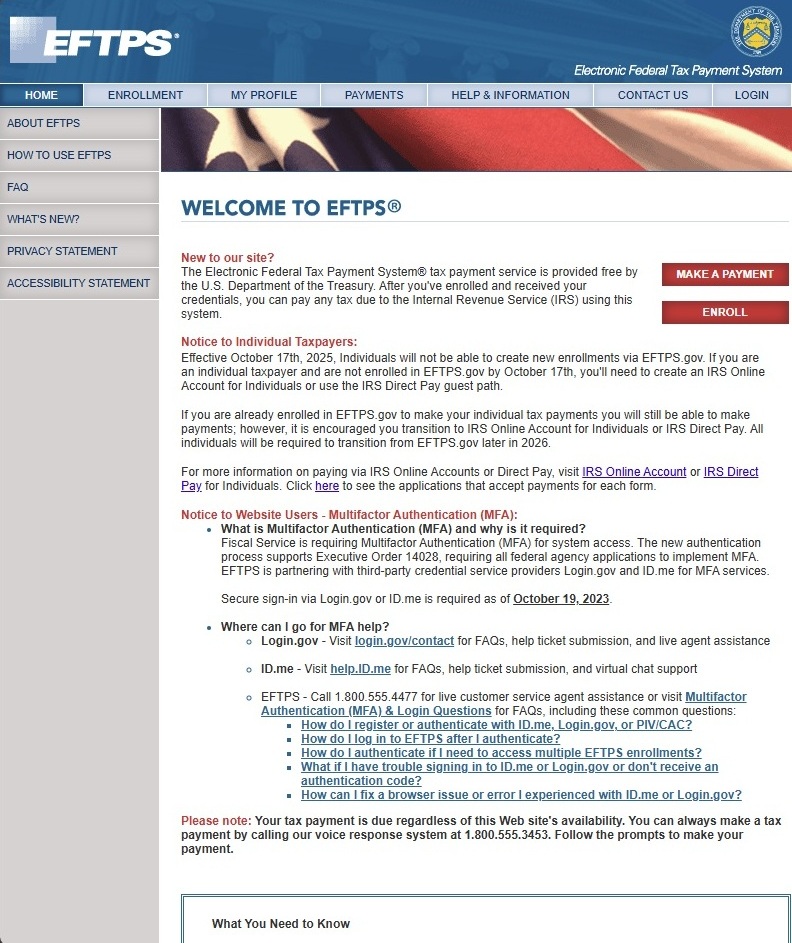

Option 3: An EFTPS account

Paying estimated taxes using an EFTPS (Electronic Federal Tax Payment System) account is highly efficient for those seeking control and flexibility in managing tax payments. It’s particularly suited for individuals who prefer scheduling payments in advance and tracking their payment history online. EFTPS provides a secure, government-run system, ensuring reliability and peace of mind. This method is ideal for both individuals and businesses looking for a consistent, organized approach to handling their tax obligations.

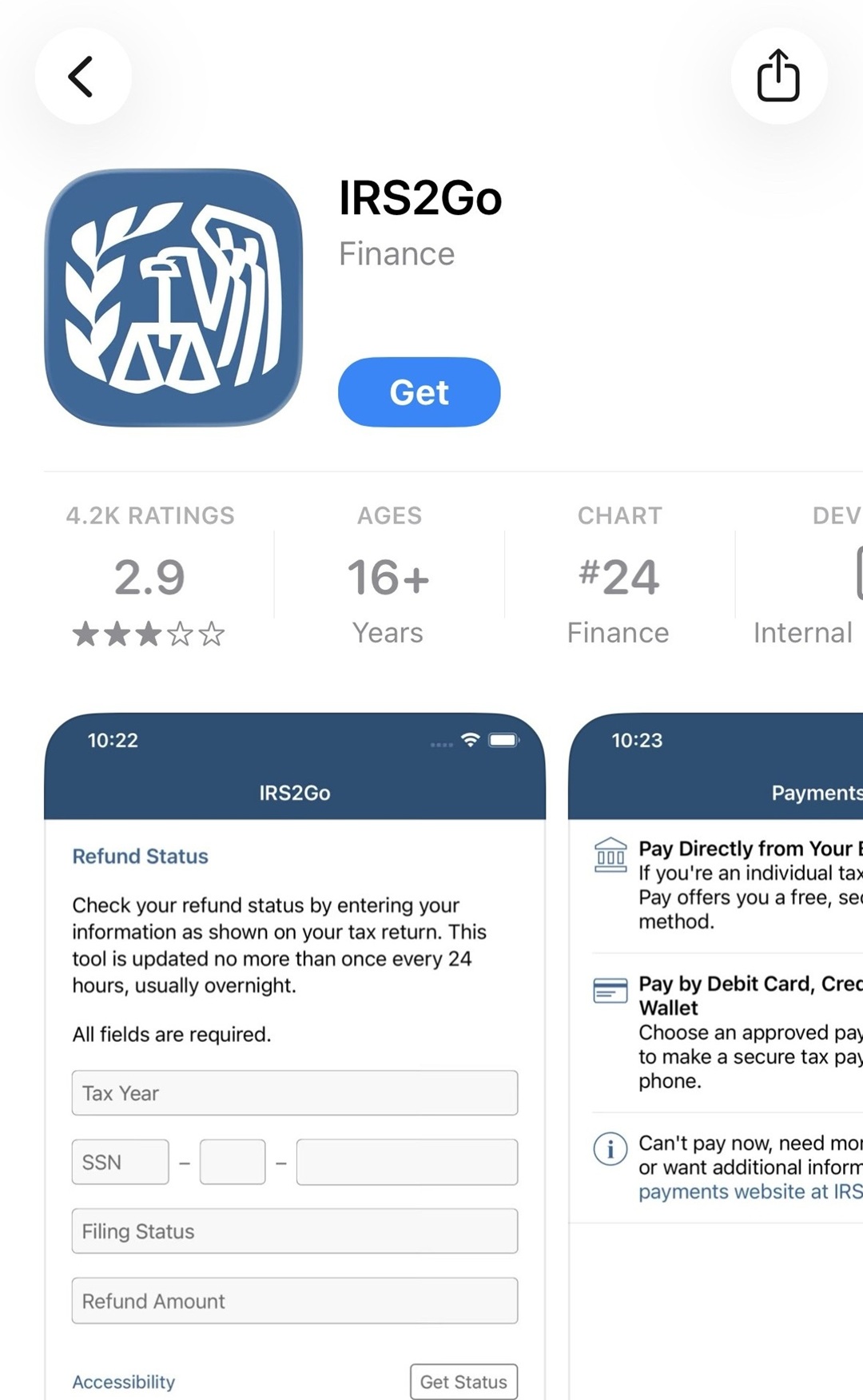

Option 4: Mobile App (IRS2Go)

Paying estimated taxes through the IRS-approved mobile app (IRS2Go) is a great choice for those who value convenience and speed. It’s ideal for tech-savvy individuals who prefer handling financial tasks on the go. With a few taps on your smartphone, you can easily pay your taxes anytime and anywhere without the need for a computer or physical mail. This method offers a user-friendly interface, instant payment confirmations, and the ability to keep track of your payments directly from your phone.

Option 5: Phone Payments

Paying estimated taxes by phone is an excellent option for those who prefer the simplicity and directness of speaking to a representative or following voice prompts, especially if they are not comfortable with online transactions or lack internet access. It’s a straightforward and accessible method, offering security and the convenience of immediate assistance and verbal confirmation, ideal for individuals who don’t use advanced technology or are wary of online security.

Option 6: Physical Check

Paying taxes by check is a traditional, straightforward method for those who prefer tangible records and are hesitant about online transactions. It’s slower than digital methods but offers a clear, documented trail for your records, making it a reliable choice for those less comfortable with technology.

Option 7: Increasing W-2 Withholdings

Paying estimated taxes by increasing W-2 withholdings is an efficient method for employed individuals. It streamlines tax payments by adjusting the tax amount withheld from your regular paycheck, reducing the need for separate quarterly payments. This approach is particularly convenient for those who prefer a set-and-forget method, ensuring tax obligations are met seamlessly throughout the year. Complete the IRS Form W-4 for your employer to withhold the correct federal income tax from your pay.

Why should you make quarterly tax payments?

Penalty Avoidance

Making quarterly estimated tax payments is crucial primarily to avoid penalties. The IRS requires that taxes on income not subject to withholding be paid as you earn it throughout the year. Failing to do so can result in underpayment penalties, which are essentially interest charges on the amount not paid on time. By making these payments quarterly, you ensure that you’re covering your tax liability as you go rather than facing a large bill and potential penalties at the end of the year. This approach helps maintain compliance with tax laws and avoids the added financial burden of penalties, making your overall tax management more predictable and stress-free.Top of Form

Peace of Mind

Paying your taxes through quarterly estimated payments offers significant peace of mind. It allows you to spread your tax liability throughout the year, avoiding the stress of a large lump-sum payment at tax time. This method of regular, smaller payments helps in better managing your cash flow and budgeting, reducing financial anxiety. Knowing that you are staying on top of your tax obligations consistently also alleviates the worry of falling behind or encountering unexpected debts during the annual tax filing season. In essence, it ensures a more controlled and predictable financial planning approach, giving you a clearer and more relaxed mindset regarding your tax responsibilities.

Improved Financial Focus

Paying estimated taxes quarterly helps in developing better financial management habits. This regular payment schedule prompts you to monitor your income and expenses more closely, leading to more disciplined budgeting and financial planning. By consistently setting aside money for taxes, you enhance your overall financial awareness and preparedness, contributing to a more stable financial situation.

The “Safe Harbor” Rule

The “safe harbor” rule in the context of quarterly estimated tax payments is an IRS guideline that helps taxpayers avoid penalties. According to this rule, if you pay either 90% of the tax you owe for the current year or 100% of the tax you paid the previous year (110% if your adjusted gross income is more than $150,000), you won’t face underpayment penalties, regardless of how much you owe when you file. Making quarterly estimated tax payments using the safe harbor rule ensures you meet these minimum requirements, providing relief from the worry of calculating exact amounts due each quarter. It simplifies tax planning, especially for those with fluctuating incomes, and offers a buffer against potential penalties.

How do I lower my taxes?

Partnering with Tax Hive can be a strategic move to help lower your tax liability and manage estimated quarterly taxes. Tax Professionals can help with tax savings plans and bookkeeping to identify potential deductions and credits you might be missing, ensuring you’re not overpaying on taxes. Schedule a free consultation to learn more about how Tax Hive can help.

To lower your taxes without professional help, consider these straightforward strategies: Increase contributions to retirement accounts like 401(k)s or IRAs to reduce taxable income. Use Health Savings Accounts if eligible, as they offer tax-free contributions and withdrawals for medical expenses. Take advantage of tax credits such as the Earned Income Tax Credit and Child Tax Credit, which directly reduce your tax bill. Itemize deductions if they exceed the standard deduction, focusing on expenses like mortgage interest and charitable donations. Lastly, adjust your tax withholdings to match your actual tax liability better, avoiding giving an interest-free loan to the government.Top of Form

FAQs

Disclaimer

This article provides general information and should not be considered professional tax advice. Tax laws and regulations can change, and individual circumstances vary, so it is crucial to consult with a qualified tax professional or the IRS for personalized guidance and to ensure compliance with current tax laws. The information presented here is accurate to the best of our knowledge at the time of writing but may not reflect the most current tax regulations or interpretations. Readers are encouraged to seek professional assistance for their specific tax situations.

Qualifying Children – Qualifying children includes any child under the age of 19 (24 if a full-time student, or any age if permanently and totally disabled), who lived with you for at least half the year, for whom you provided at least half their support, and they are your child, grandchild, stepchild, adopted child, foster child, sibling, half-sibling, step-sibling, niece, or nephew.

Qualifying Others – Qualifying others includes any dependent for whom you provide more than half their financial support, earns less than $4700 in 2023, and does not qualify as a qualifying child.

Business Income – This includes any income from businesses you actively or passively own (except for rental income and investments through stock)

Passive Rental Income – Passive rental income includes any income from short term or long term rentals you own and did not report under business income. Please note you cannot claim losses for these activities unless they are a short-term rental you actively manage or you qualify as a real estate professional. If you cannot qualify for either of those, please enter $0 or the calculation will be off.

W2 Income – W2 income includes all your earnings from jobs you work as well as from companies you own unless that income is reported in business income

Taxable Interest and Ordinary Dividends – Please exclude dividends you know qualify for capital gains treatment. Those should be reported under capital gains. All other income from dividends or interest should be reported here.

Taxable Retirement Account Distributions – This includes all income from retirement accounts except Roth style accounts. In other words include taxable distributions and exclude nontaxable distributions.

Other Taxable Income – Please do not include capital gains or income from other areas.

Short-term Capital Gains – These are capital gains income from assets you owned for less than one year.

Long-term Capital Gains – These are capital gains income from assets you owned for longer than one year, including most qualifying dividends.

Itemized Deductions – Please enter your amount of itemized deductions if you intend to use the itemized deductions instead of the standard deduction

Tax Deductions – Exclude dependent and child tax credits, meaning everything but the $2000 and $500 credits you will receive for your qualifying children and qualifying dependents. Those will be calculated for you.

Social Security Withholdings – Please enter all amounts withheld through W2s, 1099s, or other sources for your federal withholdings. These do not include your tax payments, but would include other amounts that count as payment of your tax liability.

Tax Payments – Please include all estimated tax payments you made to the IRS to cover your tax liability this year.

Ordinary Income – This includes all your income except capital gains income

Capital Gains Income – This includes your capital gains income

Ordinary Tax – This is your estimated tax on ordinary income

Capital Gains Tax – This is your estimated tax on capital gains.

Credits and Payments – This includes credits and payments you should receive to bring down your tax liability.

Balance Due – This is the balance you should pay to the IRS to cover what is estimated to be your liability based on your entries.